Getting the keys to your first home is one of life’s great moment between mortgage approval, surveys, solicitors and the small matter of finding the actual house, home insurance can feel like just one more box to tick before you can finally move in, but it’s a box worth understanding. The right cover protects what is almost certainly the biggest purchase you’ll ever make, and your mortgage lender won’t release a cent until it’s in place.

The good news once you know how it works, it’s far simpler than it looks, at Peopl Insurance walks you through everything a first-time buyer in Ireland needs to know, from when to arrange cover, to what your lender requires, to how to avoid the underinsurance trap that catches so many new homeowners.

First-time buyer home insurance checklist

Here’s the whole process briefly work through it in order:

- Once your sale agreed start getting home insurance quotes, so you know your numbers

- Confirm your rebuild cost and use the SCSI calculator or your valuer’s report (this is your buildings sum insured, not the purchase price)

- Estimate your contents value add up furniture, appliances, electronics and belongings

- Set your cover to start on your closing date so it’s live the moment ownership transfers

- Get your buildings cover in place before drawdown your lender won’t release funds without it

- Arrange your “noting of interest” the document confirming your lender’s interest is recorded on the policy

- Collect your keys fully covered from day one.

Buildings vs contents insurance: what’s the difference?

Buildings insurance covers the structure of your home: the walls, roof, floors and permanent fixtures like your fitted kitchen and bathroom. If a storm rips off part of your roof or a fire damages the structure, this is the cover that pays to repair or rebuild. This is the part your lender insists on.

Building insurance cover –

- The permanent structure: walls, roof, floors and ceilings

- Fitted kitchens, bathroom suites and built-in wardrobes

- Garages, sheds and other outbuildings

- Boundary walls, fences, gates, driveways and paths

- Damage from fire, smoke, storm, flood and escape of water (e.g. a burst pipe)

- Subsidence, heave and landslip, subject to policy terms

- Alternative accommodation if an insured event leaves your home uninhabitable

Contents insurance covers the things inside your home that you’d take with you if you moved: furniture, appliances, electronics, clothing and personal belongings. It isn’t required by your lender, but once you’ve furnished a new home, replacing everything out of your own pocket after a burglary or flood would be a serious blow.

Contents insurance typically covers:

- Furniture, beds and soft furnishings

- White goods and kitchen appliances

- TVs, laptops, games consoles and other electronics

- Clothing and everyday personal belongings

- Jewellery, watches and valuables, usually up to a single-item limit

- Loss or damage from theft, fire, storm, flood and escape of water

- Optional all-risks cover for items you take outside the home, like a phone, laptop or bike

For most first-time buyers, a combined buildings and contents policy is the most convenient route. You get both types of cover on a single policy, with one renewal date and a single point of contact, which keeps things simple while you’re settling into a new home.

What information do I need to get a home insurance quote?

Having these to hand makes the home insurance quote quick and accurate:

- Property address and Eircode

- Property type (house or apartment), construction type and the year it was built

- The number of bedrooms

- Your buildings sum insured (the rebuild cost, not the purchase price)

- An estimate of your contents value

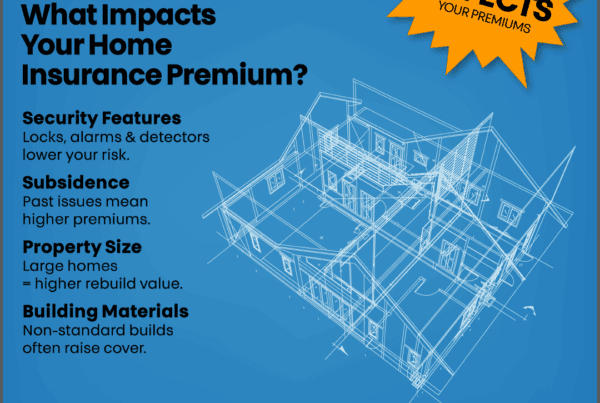

- Security features: alarm, window locks and approved door locks

- Whether the home is owner-occupied, plus any claims history

What affects your home insurance quote cover and your cost?

Two things shape every home insurance policy, what’s excluded, and what drives the price. Both are worth understanding before you buy.

What’s typically not covered in home insurance:

- Wear and tear, gradual deterioration and poor maintenance insurance covers sudden, unexpected events, not upkeep.

- Pre-existing damage that was already there before the policy started.

- Flooding where the property sits on a known flood plain, where cover may be limited or excluded.

- High-value items above the single-item limit, unless specifically listed on your policy.

- Items kept outside the home, which may be limited or excluded by default.

- Unoccupied periods many policies restrict cover if the home is empty for 30 or more consecutive days.

- Older properties may carry conditions, such as fire cover tied to the home being rewired within a set period.

What to avoid in home insurance?

The mistakes that cost first-time buyers the most:

- Underinsuring your home, guessing low on the rebuild cost can trigger the “average clause,” where your insurer reduces your payout in proportion to how underinsured you are, even on small claims.

- Insuring at market value instead of rebuild cost – They’re different figures, and only one is correct.

- A gap in cover makes future insurance harder to get and more expensive.

- Forgetting to declare changes like renovations, a home business, or plans to let or leave the property unoccupied.

- Choosing on price alone and missing key exclusions.

- Never reviewing your sum insured, even as rebuild costs rise year to year.

Get a home insurance quote with Peopl Insurance today and tick this one off your list.

FAQs

- Can I get home insurance before I’ve collected the keys?

Yes, and you should. Arrange your buildings cover so it’s active from the closing date when ownership transfers to you. You can set up the policy in advance, and have it start on the day you complete, so there’s no gap.

2. Do I need contents insurance if my home is brand new and mostly empty?

It’s worth having from the start. Even a sparsely furnished home holds appliances, electronics and the belongings you move in with, and the value adds up faster than people expect once you’re settled. You can adjust your contents sum insured as you furnish.

3. What happens to my cover if I rent out a room or work from home?

Both can change your risk profile and may need to be declared. Letting a room or running a business from the property can fall outside a standard policy, so flag it when you get your quote to make sure, you’re properly covered.

4. Does home insurance cover me while the house is being renovated?

Not always. Renovation work, especially if it leaves the property unoccupied or structurally altered, can affect your cover. Tell your insurer before work begins so they can confirm what’s included or arrange suitable cover.