Buying or building a new home in Ireland is an exciting milestone. Whether you’re stepping into your dream home or investing in a property for the future, one thing you can’t afford to overlook is property insurance.

While newly built homes may come with fewer risks than older properties, they also come with specific insurance considerations – from the importance of structural warranties to rebuild values and everything in between.

In this blog post, we’ll walk you through what you need to know about insuring a new build home in Ireland.

1. New Build Homes Still Need Insurance - From Day One

Even if your home is brand new, insurance is essential. Builders’ guarantees don’t cover everything, and lenders typically require at least mortgage protection before releasing mortgage funds. You’ll need to have buildings insurance in place before you move in – and often before completion.

2. Understand the Difference Between Buildings and Contents Insurance

- Buildings insurance covers the structure of your home: walls, roof, floors, windows, and permanent fixtures.

- Contents insurance covers personal belongings like furniture, electronics, and valuables.

For new builds, your main initial focus should be on buildings insurance, especially if you haven’t moved your belongings in yet. Once you’re settled, you can add or extend to contents cover.

3. Understanding Structural Warranty

Most new homes in Ireland come with a 10-year structural warranty from the construction company. This warranty typically covers:

- Structural defects

- Water ingress

- Poor workmanship related to construction

However, this is not a substitute for building insurance. Structural warranties often have limits and exclusions, and they do not cover fire, storm, flood damage, or theft. Your structural warranty is like an insurance on the build quality itself. But if a problem can’t be traced back to the build quality, then it won’t be covered.

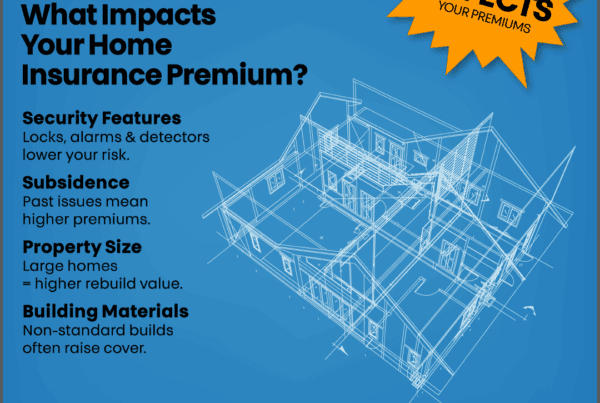

4. Accurate Rebuild Cost is Key

Insurers base buildings cover on the rebuild cost, not the market value of your home. This is the amount it would cost to rebuild the property from scratch, including materials, labour, architect fees, and site clearance.

You can use the Society of Chartered Surveyors Ireland (SCSI) rebuild calculator to estimate this, or better yet, request a professional valuation

Tip: Avoid underinsuring – it could lead to reduced payouts if you need to make a claim. The small savings on your premium aren’t worth it.

5. Energy Efficiency and Smart Tech May Reduce Premiums

New builds in Ireland often feature:

- BER A-rated energy efficiency

- Solar panels

- Heat pumps

- Smart home security

These features can sometimes lower insurance premiums, due to lower risks, maintenance costs. However the increased rebuild cost also needs to be taken into consideration.

In any case it’s vital that you inform your insurer aboutanything that could change your premium. Be sure to inform your insurer about any security systems, fire alarms and anything that raises your BER Rating.

6. Consider Optional Cover for Add-Ons

Depending on your property, you might want to include:

- Accidental damage cover (useful if you have kids or pets)

- Home emergency cover (for burst pipes, boiler breakdowns, etc.)

- Legal expenses insurance (covers legal fees for property disputes)

If you’ve built extras like a home office, garden room, or EV charging point, make sure they’re included in your policy.

7. Compare Insurers and Look for New Build-Friendly

Policies

Some insurers specialise in new builds and may offer more competitive premiums or bundled policies that suit modern homes. Use a broker or comparison tool to get quotes, but always check the policy wording carefully for:

- Exclusions

- Excess amounts

- Claim limits

Final Thoughts

A new home is a fresh start, and getting the right insurance means you can enjoy it with peace of mind. While your home may be built to the latest standards, it’s still vulnerable to fire, storm damage, or unforeseen events – and that’s where proper insurance comes in.

Make sure to:

- Get cover in place before completion.

- Calculate the correct rebuild cost.

- Include any special features or add-ons.

- Review your policy annually as your needs evolve (we’ll offer you the best deal every year based on your circumstances).

- Consider whether or not you need non-standard insurance policies for your build.